MGM Resorts International (MGM) and arch-rival Caesars Entertainment (CZR) stand out among the so-called Las Vegas Big 4 because, unlike Wynn Resorts (WYNN) and Las Vegas Sands (LVS), they have significantly smaller global footprints.

But can they sweat their domestic focus to deliver the returns investors demand?

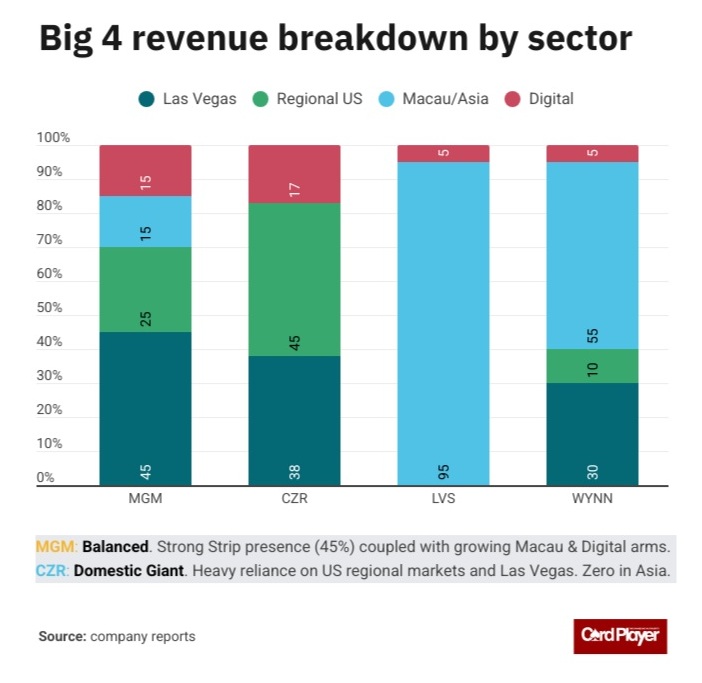

In fact, Caesars has a tiny footprint in Macau and other parts of Asia. On the other hand, MGM Resorts does, but with a far smaller revenue attribution than Las Vegas Sands.

Las Vegas Sands has essentially exited the US. The company derives more than 90% of its revenue from Macau/Asia. Lastly, Wynn Resorts generates about 50% of its total revenue from Macau/Asia.

Between MGM and Caesars, the former has much greater visibility in the digital betting world, with a strong sports betting profile. In contrast, Caesars is known for its domination of the Las Vegas Strip. Additionally, Caesars’ sticky rewards program performs as the glue that binds its 50-plus properties.

How Much Are Tariffs Dimming Las Vegas’ Sparkle?

MGM Resorts CEO Bill Hornbuckle stated in remarks accompanying the Q1 2025 results that he didn’t expect to see much of an impact from tariffs, citing Vegas resilience.

But Caesars CEO Tom Reeg said a drop in Canadian visitors were at least partly responsible for the softness his company saw during the Las Vegas summer months. Reeg credited tariffs as as a driver of the tourism dip.

The stock prices of all the Las Vegas Big 4 plummeted on April 3 (dubbed ‘Liberation Day’) when President Donald Trump announced sweeping tariffs. Those specific tariffs were later rolled back.

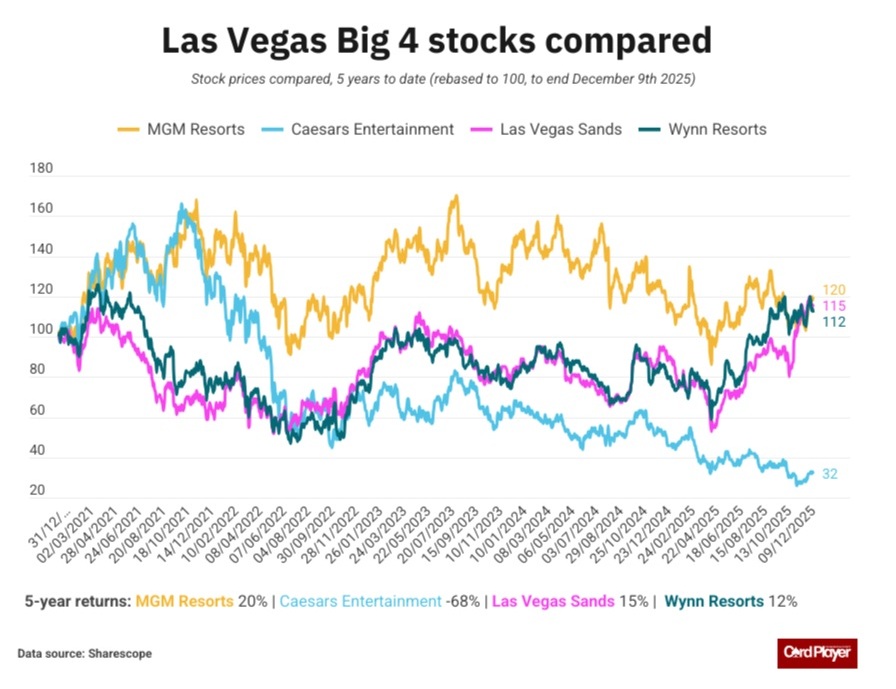

Not surprisingly, the stocks with the majority of their revenue originating outside the US (LVS and WYNN) performed the best. At the same time, Caesars, with no meaningful overseas footprint, fared the worst. Its share price fell 68% in the past five years.

MGM Covers Its Bases, Unlike Caesars

MGM Resorts, which recently withdrew from the race to open a casino in New York City, also offers a reward program – one that was significantly strengthened in 2024 thanks to its lash up with Marriott Bonvoy. The partnership provides access to Marriott’s database of leisure and business travelers worldwide. As a result, MGM lowered its customers acquisition costs.

With brands such as Bellagio, ARIA, Vdara, The Cosmopolitan in the luxury tier, a core premier tier catered for by MGM Grand, Mandalay Bay, Park MGM; mass market customers targeted by New York-New York, Luxor, Excalibur; and a regional and international segment served by the likes of Borgata and MGM Macau (majority-owned Hong Kong listed subsidiary), respectively, MGM Resorts could be said to cover all the bases.

Caesars perhaps takes a less stratified approach, but with a strong regional spread as special protection and cultivation of its Las Vegas profile. Caesars Palace remains the undisputed flagship of the group.

Its regional portfolio extends from the plains of Iowa to the bustle of New Orleans. Harrah’s and Horseshoe are the key brands of the regional business.

The watchword for these brands is operational efficiency, where Eldorado’s business strategy of acquiring casinos and turning them into lean margin-enhancing machines comes into its own.

Caesars’ so-called Las Vegas Cluster remains the core of the business. The company owns the industry’s original and largest loyalty program (60 million members), which provides it with a database that enables it to cross-sell at a regional level. Thus, it funnels customers from its regional properties to Las Vegas.

The Las Vegas Cluster stands in contrast to MGM Resorts’ positioning to capitalize on the US tourism industry’s popular travel routes, collectively known as the ‘Golden Triangle’ (San Francisco, Los Angeles, Las Vegas).

Las Vegas Sands & Wynn Resorts Win In Asia, Caesars & MGM Burn Cash

In addition to their Asia exposure, the other two components of the Big 4, Las Vegas Sands and Wynn Resorts, also have distinctive brand strategies to differentiate themselves in the marketplace.

In fact, Sands exited the digital gambling market as it doubles down on Asia. Las Vegas Sands targets business tourism (MICE – Meetings, Incentives, Conferences, and Exhibitions and the mass market).

Wynn Resorts eschews the budget end of the market entirely. It concentrates on the high-end luxury demographic and premium mass segment.

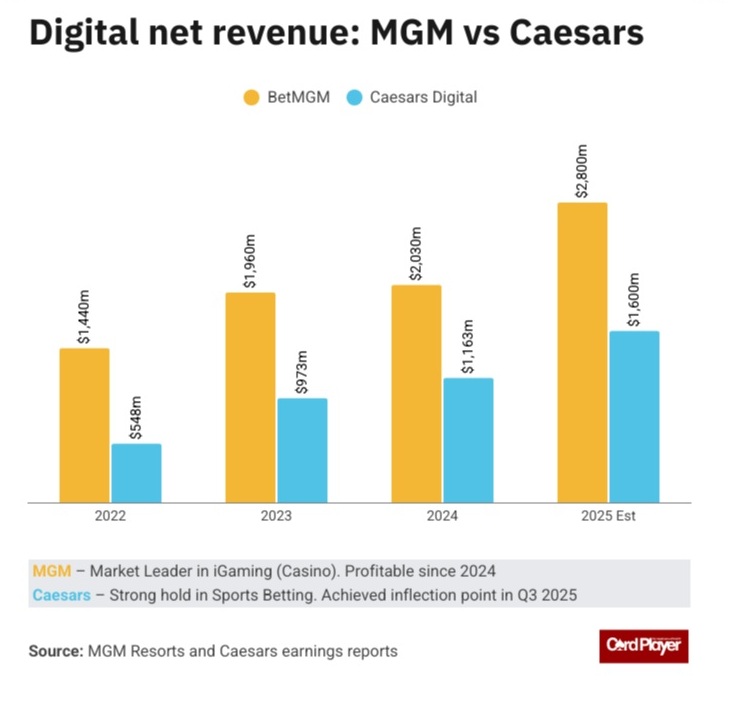

Third quarter 2025 results highlight the varying strategic trajectories of MGM Resorts and Caesars. BetMGM achieved 23% digital growth for the parent group, despite facing operational headwinds in Las Vegas.

On the other hand, Caesars increased revenues by a mere 1% to $8.57 billion, reducing net loss by 13% to $252 million. Notably, it has made some progress in reducing its $24 billion debt burden. There was a net decrease in interest expense of 5% to $1.75 billion.

How did Caesars pile on the debt? In 2008, Apollo Global Management and TPG orchestrated a leveraged buyout that saddled the company with substantial debt. Then, the $17.3 billion acquisition of Caesars Entertainment by Eldorado Resorts added to the debt, which had become even more burdensome, following the losses accumulated in the wake of the 2008 recession and the subsequent downturn in consumer spending.

COVID Causes Differences Between Companies

When the COVID pandemic hit in 2020, the two companies found themselves in starkly contrasting financial positions. The COVID-19 lockdowns shuttered the hospitality and entertainment industries, including casinos. Both companies burned through cash due to their fixed costs, resulting in a net loss of $1.8 billion for Caesars, while MGM saw net revenues in 2020 collapse by 61% in Las Vegas and 77% in China.

However, MGM’s much stronger financials meant it avoided the trauma faced by Caesars on the back of its Eldorado merger debt burden – that deal closed mid-2020.

From COVID Recovery To Digital Futures?

The advent of the vaccine rollout and the subsequent lifting of restrictions led to a strong bounce back. MGM’s Las Vegas revenues jumped 111% year on year, with adjusted property EBITDA topping $1.7 billion as pent-up demand was unleashed.

Meanwhile, Caesars’ EBITDA surged to $1.96 billion, although a significant portion of that had to be allocated towards paying down the substantial debt pile. China didn’t end its ‘Zero Covid’ lockdown restrictions until January 2023, which. When the policy ended, it proved particularly impactful on the diverging strategies of the two firms.

China’s reopening in 2023 was a boon for MGM Resorts. MGM China revenue growth came in at 28% year on year, reaching $4 billion, of which $1.1 billion was attributable to its Macau operations. This development proved exceptionally fortuitous, as it coincided with a flattening in US growth.

The previous year, in 2022, it was apparent that MGM had started to aggressively implement a plan to offload its casino real estate interests, completing the sale of MGM Growth Properties to VICI Properties for $4.4 billion in a cash-and-debt deal. In the same year, MGM acquired the operation of The Cosmopolitan ($1.6 billion) as part of its strategy to boost its luxury offering. That left it with substantial lease obligations, but still an enviable balance sheet when viewed from Caesars’ perspective.

Where the companies’ approaches aligned was in the digital realm, with both investing heavily to capture market share. For instance, Caesars lost $666 million, mainly due to its marketing efforts aimed at attracting digital customers. MGM’s joint venture with Entain, BetMGM, racked up losses, as did its other JVs, such as the tie-up with Grupo Globo to break into the Brazilian iGaming market.

Asia Drives MGM’s Growth

At Caesars, there was, at last, some good news. After posting a huge loss in 2022, EBITDA turned positive in 2023, coming in at $38 million for the year. Restless investors had also demanded dramatic cost-cutting measures, to which the board acquiesced.

But it was Caesars’ exclusively domestic focus that has come more to the forefront as an area of weakness.

MGM was able to report record 12-month net revenues of $17.2 billion last year (2024). Those figures represented a 7% improvement on the previous year.

Drilling down into the results, Las Vegas revenues were essentially unchanged at $8.8 billion. Nearly all of the upside came from MGM China’s Macau operations. Investors were further cheered by a buyback of 33 million shares, returning $1.4 billion to shareholders. It announced another buyback program in April this year worth $2 billion.

It was a different story at Caesars, which recorded a net loss of $278 million on $11.2 billion in net revenue, a slight decrease from 2023. The lack of an Asian net income generator became more glaring. Interest expenses on that debt mountain didn’t help the bottom line either.

Caesars does have an international footprint. Its modest revenue contribution is reported in the “managed and branded” segment ($274 million, down from $307 million in 2023).

MGM & Caesars In The Big 4’s Strategic Positioning

Despite Headwinds, Significant Upside Ahead For MGM & CZR

MGM Resorts and Caesars Entertainment are facing domestic headwinds, which could worsen if the Trump administration goes ahead with its latest plans to tighten entry restrictions, including for non-visa countries such as the UK and Germany.

Flights from Canada into the US are already down significantly, so additional travel restrictions on international travelers will not help cash flow on The Strip, threatening to take the shine off the hoped-for revenue bump from the 2026 soccer World Cup.

Complaints about exorbitant price hikes and hold rates on slots creeping up are not helping to sell Vegas to the masses. The dynamic pricing of hotel rooms at the MGM Grand and Caesars Palace is not going over well. Neither are stories about Las Vegas visitors being charged $33 for a bagel and a cup of coffee.

Bosses got some heat on recent earnings calls concerning the alleged price gouging. Caesars’ Reeg admitted, “I don’t discount that there are areas in our business and in Las Vegas that might have gotten over their skis pricing-wise.” Hornbuckle at MGM held his hands up too, responding, “Shame on us” when challenged about eye-watering prices.

And none of this penny(dollar?)-pinching is bolstering operational efficiency.

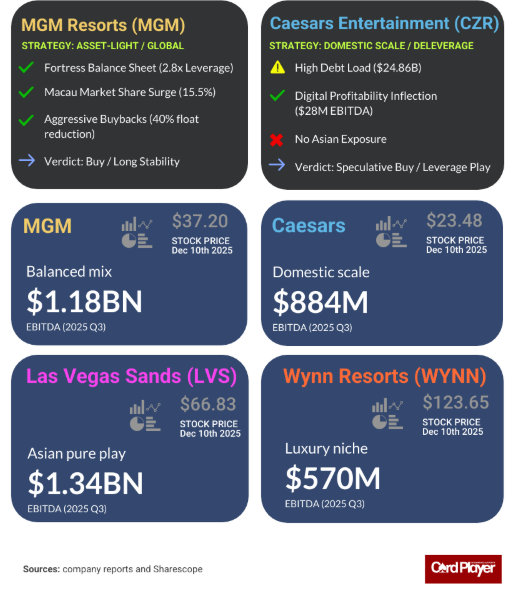

The return on equity (ROE) for Las Vegas Sands is 66%, achieved on an operating margin of 24%. In stark contrast, Caesars Entertainment has a negative ROE of -4%, in a reflection of its debt overhang. MGM’s ROE is better, at 10% but leaves plenty of room for improvement.

Caesars’ Weakness Provides Better Value

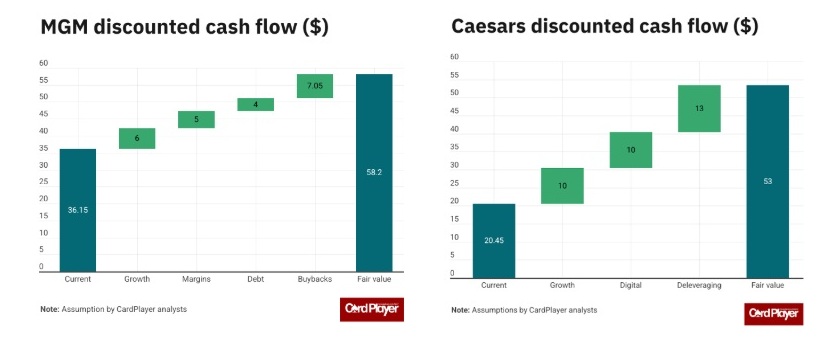

Our discounted cash flow (DCF) analysis reveals significant valuation disconnects. Caesars Entertainment shows the highest upside (159%) due to current negative market sentiment about its debt levels, despite operational improvements. MGM’s 61% upside reflects temporary Q3 headwinds that mask underlying digital growth potential and its Macau expansion plans coming on stream early next year.

We rate MGM a buy. Its diversity provides stability. However, Caesars has the greater upside potential because it is coming from a weaker position. For those with the risk appetite, CZR is a speculative buy, depending on how it progresses in its deleveraging mission. For both companies, their domestic footprint means performance is dependent on how tourism performs in the US going forward.

Still, Las Vegas has been counted out before, so a savvy investor would probably bank on resilience coming through yet again. With the World Cup approaching and digital media continuing to grow, the risk-reward ratio reflected in our DCF models highlights the potential money on the table.